Exogeneous exchange rates

Theory and empirics of a Clark medal insight

|

|

When on April 16 news broke that Oleg Itskhoki had received the 2022 Clark medal hardly anyone bar the recipient himself could have been more excited than yours truly. This excitemtent is caused by the American Economic Association's (AEA) recognition of Itskhoki's achievements which really have the potential to mark a key milestone towards a truly human-centred economics science. Though there still is a long way to go a first important brick in the ontological wall may have finally given in to let some faint light shine through.

In lauding the Clark medallist's works, the AEA, who awards the medal to outstanding economists under the age of forty who work in the US, emphasises that

"The key insight is the recognition that financial market noise, not economic fundamentals, may be the main driver of exchange rates."

It is very difficult to underestimate the implications of this approach as it means no less than putting economic analysis back on its feet. So far, mainstream economics has it that asset prices such as exchange rates or stock prices are accessible to science-like modeling by linking them to measures like export and import, interest rate differentials and other "economic fundamentals". Itskhoki, by contrast, now dismisses all these "fundamentals". And so yours truly has been doing since many years ago.

The year 2005 saw the start of a series of presentations1 and publications about one main theme: the impossibility to model asset prices as a function of "economic fundamentals". Yet instead of referring to vague "financial market noise" as the source of exchange rate movements, it is more adequate and concise to think of human agency, human's signature feature of being able to define, express and pursue one's own will, to be this "noise".

In order to support the idea of human dominance, or the dominance of "noise" in AEA slang, a 2008 piece titled "Rationally 'irrational': Theory and empirical evidence"2 develops an asset pricing model in which humans take centre stage. In this model higher trading activity increases volatility IF humans act idiosyncratically. If, however, they are aligned by some "fundamentals" the variance converges to a fixed number. Empirical evidence clearly favours idiosyncrasy of humans since increased trading activity is associated with elevated asset price volatility.

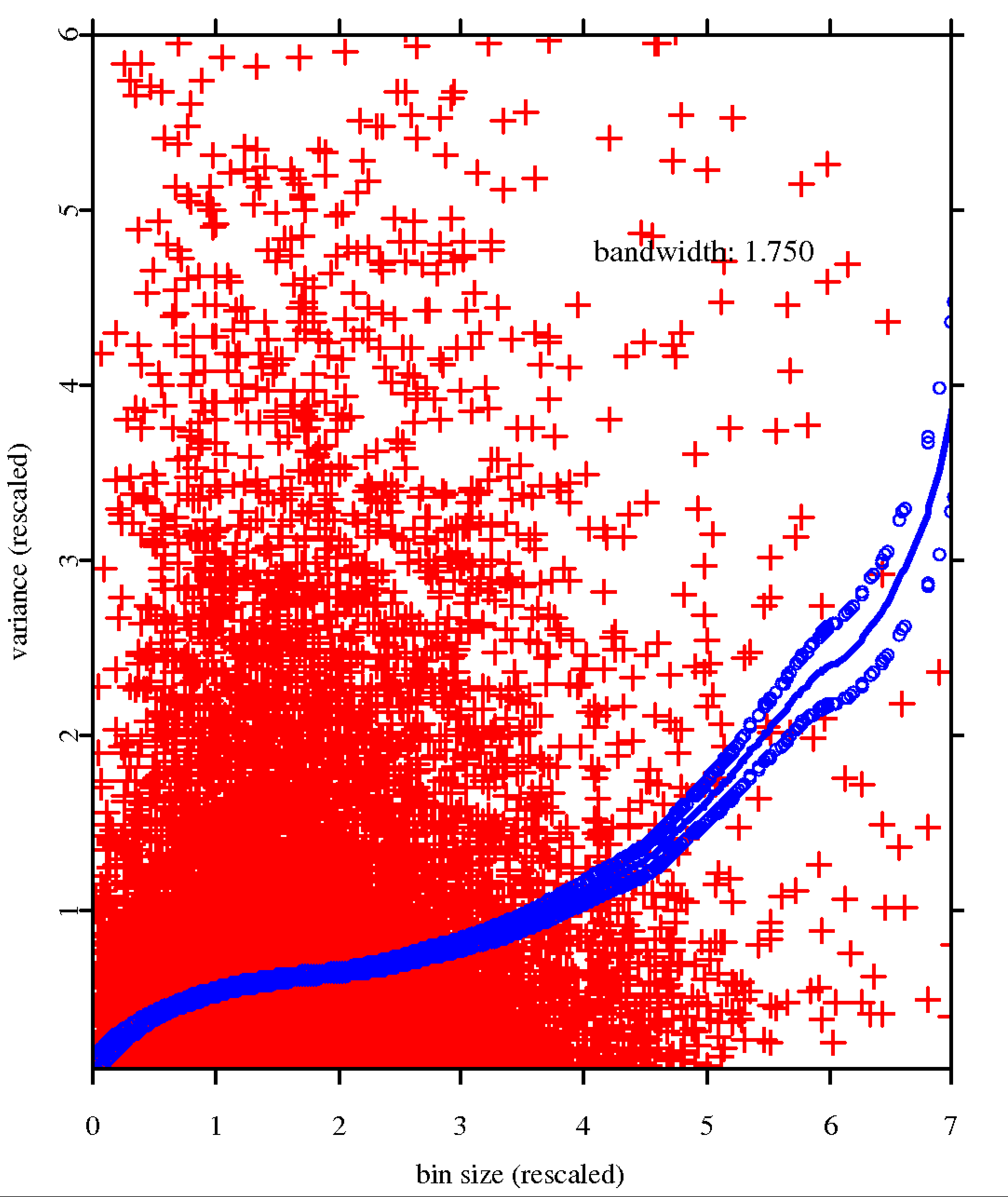

source: Puzzle solver, p. 46.

Returning to the medallist, Itskhoki directs the power of his insight against so-called "puzzles" among which the "uncovered interest parity puzzle" is exceptionally notorious. Picking and winning a fight with it like Itskhoki did, therefore, has to be considered a major achievement.

The puzzling problem to be resolved can be cast in this single equation:

This equation says that the interest rate differential between two countries () and the expected appreciation of the exchange rate () should add up to some (zero mean) error term () if traditional economic logic applies to the determination of flexible exchange rates.

In his paper "Exchange rate disconnect in general equilibrium", Oleg Itskhoki shows, however, that when allowing this error term to exhibit (near) non-stationary behaviour the "uncovered interest parity puzzle" disappears from an international macro model of the dynamic stochastic general equilibrium type together with a whole bunch of other puzzles.

Non-stationarity of the error term is defined as the secular increase of its variance over time and implies, therefore, no less than the impossibility to establish an economically meaningful link between the "fundamental" interest rates and the exchange rate. Itskhoki further argues that more than anything else picks up "noise trader shocks" eventually rendering the error term nonstationary.

It is hence this "noise", the inexplicable part of human action, which causes the non-stationarity and thus catches all there is for explaining the exchange rate.

The truly revolutionary element in Itskhoki's reasoning, therefore, is to let go of a long-standing and cherished belief in the links between "fundamentals" and the exchange rate. Rather, it is by not enforcing such a bond that resolves quite a few puzzles at once. In other words, severing the traditional mainstream links is a true "Puzzle solver" (2009).

The above picture is borrowed from the said 2009 working paper and illustrates empirically that no such link does in fact exist. The variance of (denoted in equation (7) on p. 27 in "Puzzle solver") does instead increase the more traders are active. This correspondence between trading activity ("noise trading" according to Itskhoki) and is thus born out by actual data and should be considered the root cause of the well-established random walk (non-stationary) and hence "puzzling" behaviour of the error term.

Pitching the inflating variance of the error term against canonical macro puzzles really adds to our understanding of the economy because it shows that attempts (by economists) to picture human's free will as being controlled by economic logic are in vain. An interesting and instructive attempt to nevertheless do exactly that is owed to C. Engels (2016)3 who duly fails, however, dubbing his failure as (yet another) puzzle. Building on his main insight Itskhoki handily shows that also this puzzle can be resolved.

Busting puzzles is not the end of the story, however. The recognition of the role of market "noise" or, rather, human agency, has very far reaching consequences for the practice of economics. A first one is how economists should model the economy because when accounting for human agency,

or, in other words, human agency ("noise") drives economic fundamentals and not the other way round."a straightforward feedback from macroeconomic conditions to exchange rates does no longer exist" (Our economy, p. 573),

The second implication reaches even further. Accepting "noise" as a key driver of economic fundamentals is an important intermediate stop on the way towards an appropriate, productive ontology of economics.

The current dominant ontology in economics with its equilibrium obsession, neatly defined fundamentals, distribution functions, decision rules, etc. suits natural science problems very well but has little or no connection to actual human behaviour because - as Itskhoki has nicely demonstrated - human behaviour is dominated by "noise" and evades natural science-like modeling.

Apparently, as of 2022 neither the AEA nor Oleg Itskhoki fully embrace these second, profound implications of the Clark medallist's research results. But for two reasons that is not as bad as it may sound. First, the AEA acknowledges that Itskhoki's insights set a framework for "thinking about exchange rate analysis"4 rather than marking the end of a road.

The second reason for optimism is that it took only roughly 15 years from pointing out the puzzle busting powers of genuine "noise" for the first time5 until their eventual general recognition via the Clark medal award.

Therefore, also the deeper insights might well become mainstream in the foreseeable future and economists are well-advised to keep a close eye on the coming Clark medallists if they don't want to run the risk of missing out on fantastic excitement.

Yours truly's PhD supervisor attended one of the first presentations and expressed his firm belief that the main insight would never be accepted by the economic community (he himself included) and certainly not within the ten years or so yours truly predicted.

All of yours truly's working papers and articles (save the book) linked to on this page have been submitted to - and duly rejected by - the AER for publication at some stage.

See Engels, C. (2016):"Exchange Rates, Interest Rates, and the Risk Premium," American Economic Review, 106(2), 436–474.

See https://www.aeaweb.org/about-aea/honors-awards/bates-clark/oleg-itskhoki. (17 April 2022)

Yours truly firmly believes that the whole issue is so obvious that there surely have been others who found out even sooner. Many candidates are quoted in my book Uncertainty and Economics.